sobeit69

Well-Known Member

Oh I’m sure it was....they are scumHas to be Napletons.

Sponsored

Oh I’m sure it was....they are scumHas to be Napletons.

By law you can not make someone make X amount of payments, arrange for other financing thru a credit union and they will pay it off right away, I have done this and it screws the finance manager right up the ass when they clawback the bonus he got the month before.Hey Chocolate,

I'm with you and that's what I was going to do, but he made it very clear I was committed for at least 6 payments. I didn't get far enough to read the "fine print" and I was fairly pissed by that point. So I walked. I called them out on the bait and switch; nothing but crickets so far. I don't think they really care; they'll undoubtedly find someone who doesn't mind paying the finance charge. But one thing is clear: they are NOT selling a Jeep for under invoice, they get their money back through the finance scheme.

I believe in FCA financing in the agreement your obligated to 6 months from what I've been told !Take the Jeep at that price with their crappy financing. Go straight home and refinance with the lender of your choice or pay it in full if that’s what you want to do. Two can play that game.

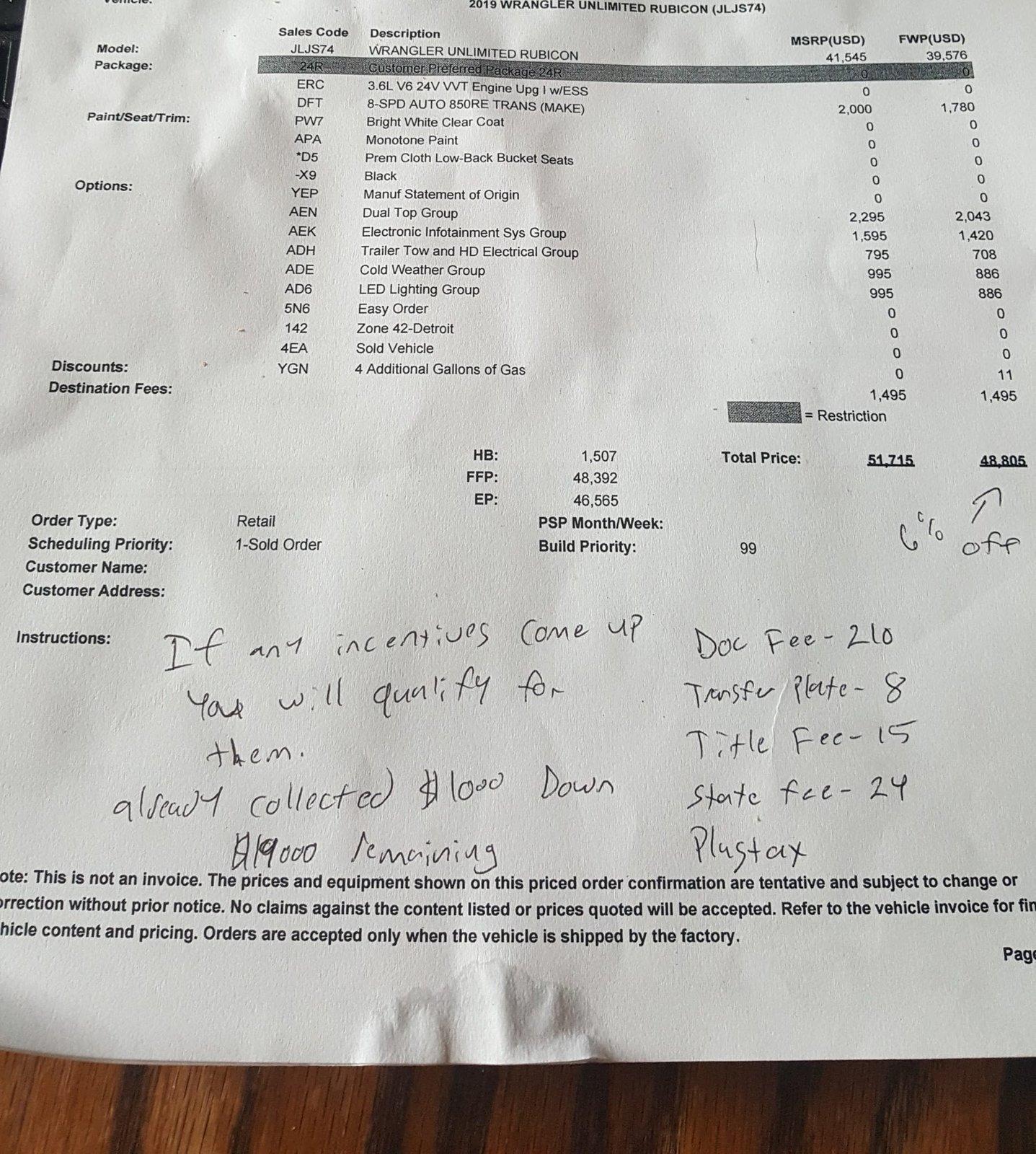

I think you got 6% under msrp, not invoiceI was going to drive go out of state to buy a JLUR but thought there has to be a better way. This is what I did. My goal was 6% under invoice. I did a Google search of Jeep Dealerships in Michigan. Then I started calling Sales Managers from closest to me and worked my way out. This is what I said:

I am ordering a Rubicon Unlimited. I have a great credit score, will be putting 20,000 down, if you will do 6% under invoice, I will come and put down a deposit and order it. I know exactly what I want and will send the details to you. A dealer 70 miles from my home said send me what you want and I will call you right back. I texted him what I wanted and he called me back and said lets do this.

I drove down gave him 1000 down and he ordered my JLUR. I was at the dealership about 15 minutes. The thing that took the longest was getting the receipt for the 1000 dollars. When the JLUR came in. I told him that I would finance through the dealership if he was able to beat the best rate I could find. He did beat my rate by a small margin. I came and picked up the JLUR and was at the dealership under an hour. I signed the papers and a salesman showed me the basics of the JLUR and I was out the door.

This is the deal that I got.

MSRP was $51715. I paid 6% off of the $48805.I think you got 6% under msrp, not invoice

Heuer: This is helpful information. I guess my concern with Kent is that he can't give me any idea what the rates would be at delivery time and I'd kind of like to have some idea before I commit to order from him. Did you know some ballpark numbers before you even ordered?I picked up custom ordered rig from Kent last week. They were very up front about the fact that I’m not legally bound to the financing and can refi at any time and they are asking that I don’t, but I could if I wanted. I never once felt like they were trying anything shady and they provided all of the numbers prior to my flight there. The financing is also not necessarily through FCA, national lenders like Wells Fargo are also considered.

I had looked at their website briefly a few months ago but couldn’t find what I wanted so I custom ordered. I can see how some would be pissed if they looked at the website and had a surprise when it came time to sign. Buyer beware, and just like with any major purchase always ask a lot of questions and read the fine print whether it’s from them or a different dealer

So true. They are trained to find your biggest concern (and weakness), whether it be the sales price, the offer for your trade or your monthly payment. They can screw you over in any of these categories as well as having outrageous documentation fees. Buyers beware. Do your homework BEFORE showing up at the dealership. But, after all, it's just SALES 101. Any time you can increase the emotional desire to purchase, logical thinking starts to take a back seat, right?Whenever I buy a vehicle, which is generally once a decade I always leave off my SSN. The salesperson will say I forgot it and I always let them know that nothing matters if the price of the vehicle isn’t right. They get plenty of people who pay for all the dealer mandated add-ons, but I am not one of them. The sales people are trained to focus on monthly payments and then ramp up the terms and rates to maximize the profits for the dealership. An old trick my dad told me was when they ask you what color you want, tell them the cheapest one. They want to get you saying yes so it becomes an emotionally driven event and you will accept a higher price. Be like Spock and stay logical. If the deal isn’t good walk away.

They can not “make you make 6 payments” it’s against the lawI believe in FCA financing in the agreement you obligated to 6 months from what I've been told !

WE GET TO FINANCING.

New to the forum. Never owned a Jeep before, so my learning curve here has been steep. Thanks to all of you who have the knowledge and take the time to post very useful threads for "noobs" like myself.

I'm real close to purchasing a new Rubicon 2 -door, but so far have been disappointed with the truthfulness of local dealers; especially their websites. Even more disappointing is that some of the dealers (Idaho) have been praised by forum members who have traveled across country to get below invoice pricing. That has not been my experience so for. This was my experience this weekend.

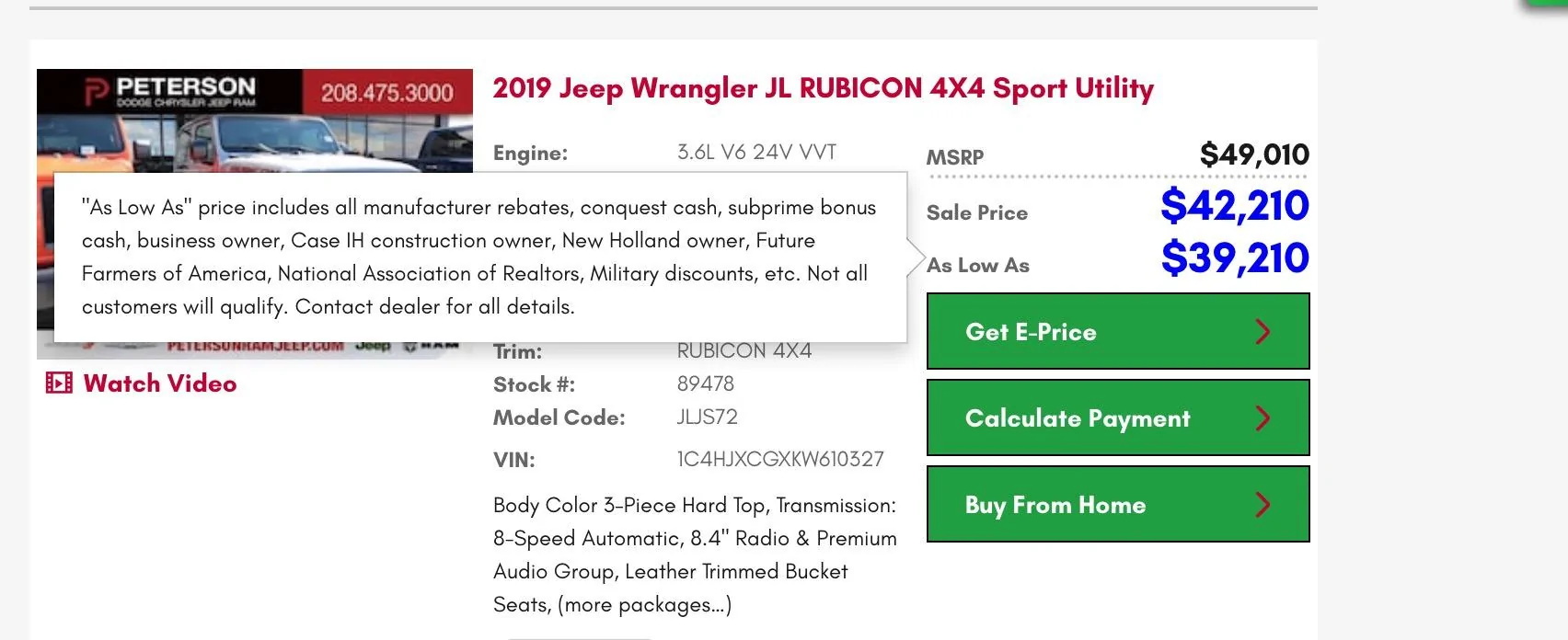

I go to Peterson Jeep in Nampa Idaho. After all, there are some very positive reviews about them here. They have a Rubicon which is advertised @ is $42,210 ("Sale Price"); the MSRP is $49,010. That's approximately 13.8% below MSRP, or 8% below invoice. Seems like a good deal. I'm ready to buy; seems like a fair deal and inline with what others have posted. Not so fast. Finance guy comes out and says "well in order to get that price, you have to let me get the financing." His financing rate is over 10% (I'm assuming through Chrysler). You gotta be kidding me.........no way am I doing that. He won't even allow me to put any money down; he absolutely refuses to sell me the Jeep at the "Sale Price" even if I pay cash! If I want to do that, then he's going to raise the price $2,500. That would make the Jeep over invoice price. I also qualify for the Military Rebate (retired), but he says that's included in the "Sale Price" which it clearly states on their website is not the case; there is a "As Low As" sale price which takes into consideration manufacturer rebates. I would think that IF in order to get the "Sale Price" you have to finance through their lender, that should be clearly stated in the Ad on the website...........right? Which it's not, because that clearly changes everything.

Also, when you do finance through them, you agree to make at least 6 payments. At 10+% that equates to $409/month in interest. Interestingly, that is about $2500 in finance charges (over 6 months), so I suppose that's where they justify raising the price $2,500 if you put any money down. Crazy, I've never heard of a dealer NOT wanting you (or requiring) to put money down. Here's the ad:

I've read posts by others who have a positive experience with Peterson. I'm just curious if they told the entire story.................like financing for example. I'm not sure which is more disappointing, their misleading advertising, or the fact that they think I'm so stupid to go for such a bad deal.

Great first post, huh? Thanks for allowing me to vent and to you guys who are willing to pass along your knowledge.

If you sign a finance agreement contract stating that you would be in some cases there are penalties for early pay off on loans. That why you always read before you sign !They can not “make you make 6 payments” it’s against the law

It is illegal to require a set amount of payments or charge a penalty on early payoff. If a dealership if putting this in their finance/sales agreement it could be used as evidence against them.If you sign a finance agreement contract stating that you would be in some cases there are penalties for early pay off on loans. That why you always read before you sign !

The fine print counts, Retail Loans might have certain protections, but car "loans" might be in another category, which is why the lender can charge " usurious" interest rates, and have pre-payment penalties.It is illegal to require a set amount of payments or charge a penalty on early payoff. If a dealership if putting this in their finance/sales agreement it could be used as evidence against them.