cbrenthus

Well-Known Member

Lots of people make this way harder than it is, and get so worried about getting the best possible deal that they drive themselves nuts. Here are the simple steps to follow that have never failed me:

1. If you have a trade, get a reasonable value by checking KBB, current similar listings, and ebay completed listings.

2. Find the vehicle you want, and what you think the price should be

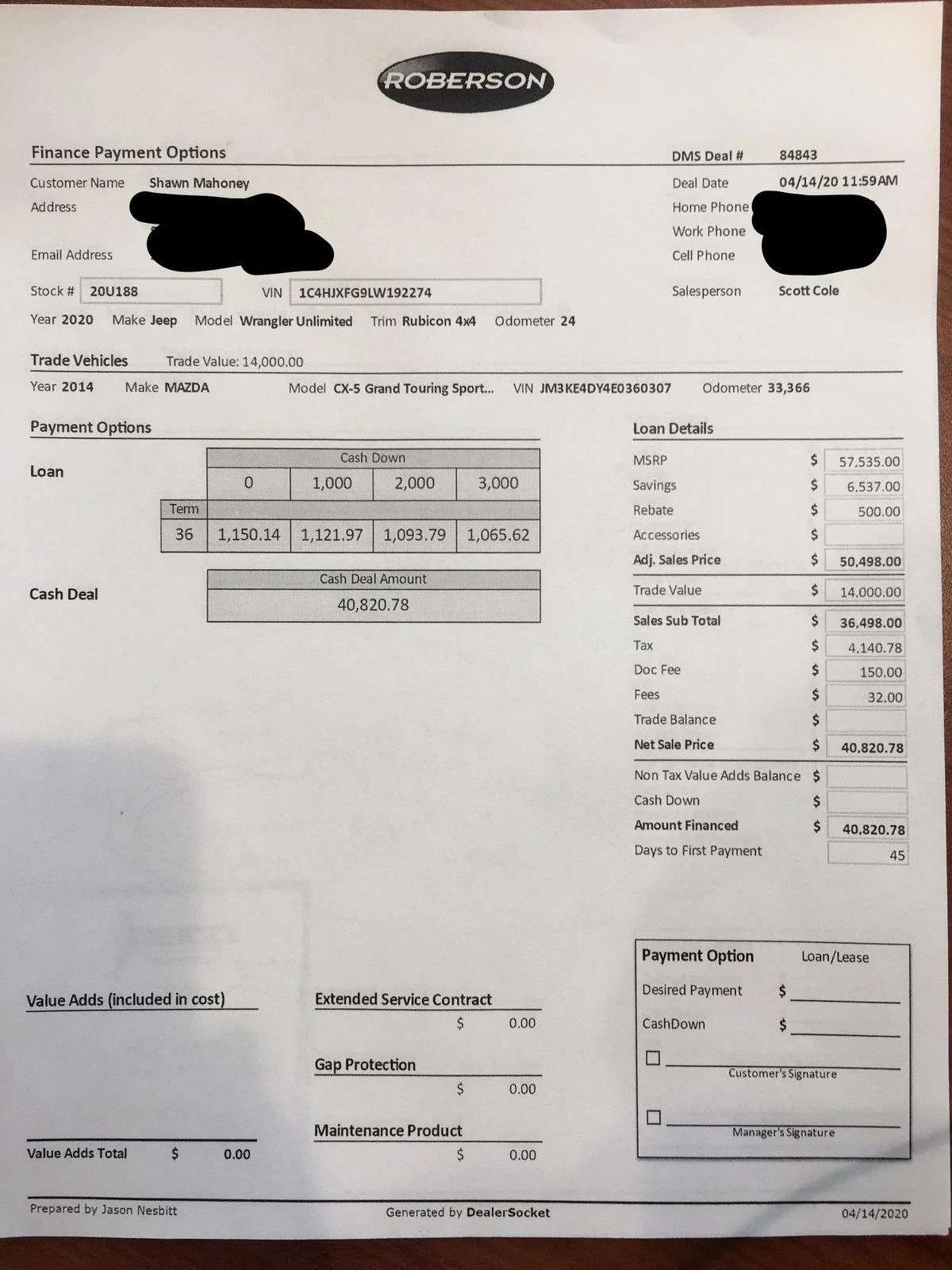

3. Figure out the OUT THE DOOR Price - take the price you think it should be, add in a little something for dealer doc fees (~$500), subtract your trade in and add in tax (many states don't charge tax on the trade in value), and then add any payoff on the trade.

4. If financing, get preapprved and have your interest rate and terms

5. Go to the dealer if local, if far then you can call but showing up ready to buy holds a lot more weight. Tell the sales guy "I have this vehicle for a trade with this payoff and if you can put me in that vehicle for X amount OUT THE DOOR I'll buy it right now."

6. When appropriate, bring up the fact that you're already approved at x amount interest for x months, but you'll let them try to beat it.

7. Get their number, and either buy the vehicle or walk away.

Tips:

Be prepared to go a little higher than what you ask for - if you're telling them $30K, and its the EXACT vehicle you want, are you really going to walk away for $75.32? What about $500?

Remember that it is better to pay a little more for what you really want than get a great deal on something you didn't really want, maybe you hate the color, or wish you had gotten a hard top instead of a soft top - you're going to live with that for the next several years.

Most importantly DO NOT stress over the added fees or your trade value - the OUT THE DOOR price is the ONLY thing that matters. One dealer might give you $2K more for your trade, but is still $1K more out the door. Another dealer might charge $1500 in fees, but still has the best OTD price around. Who cares what the fees are - it's really only the bottom line that matters.

Also, I didn't read the whole thread so I apologize if I'm repeating anything,

1. If you have a trade, get a reasonable value by checking KBB, current similar listings, and ebay completed listings.

2. Find the vehicle you want, and what you think the price should be

3. Figure out the OUT THE DOOR Price - take the price you think it should be, add in a little something for dealer doc fees (~$500), subtract your trade in and add in tax (many states don't charge tax on the trade in value), and then add any payoff on the trade.

4. If financing, get preapprved and have your interest rate and terms

5. Go to the dealer if local, if far then you can call but showing up ready to buy holds a lot more weight. Tell the sales guy "I have this vehicle for a trade with this payoff and if you can put me in that vehicle for X amount OUT THE DOOR I'll buy it right now."

6. When appropriate, bring up the fact that you're already approved at x amount interest for x months, but you'll let them try to beat it.

7. Get their number, and either buy the vehicle or walk away.

Tips:

Be prepared to go a little higher than what you ask for - if you're telling them $30K, and its the EXACT vehicle you want, are you really going to walk away for $75.32? What about $500?

Remember that it is better to pay a little more for what you really want than get a great deal on something you didn't really want, maybe you hate the color, or wish you had gotten a hard top instead of a soft top - you're going to live with that for the next several years.

Most importantly DO NOT stress over the added fees or your trade value - the OUT THE DOOR price is the ONLY thing that matters. One dealer might give you $2K more for your trade, but is still $1K more out the door. Another dealer might charge $1500 in fees, but still has the best OTD price around. Who cares what the fees are - it's really only the bottom line that matters.

Also, I didn't read the whole thread so I apologize if I'm repeating anything,

Sponsored

")