Mjmi69

Well-Known Member

- First Name

- Michael

- Joined

- May 17, 2018

- Threads

- 4

- Messages

- 332

- Reaction score

- 206

- Location

- Cornelius, NC

- Vehicle(s)

- 2019 Jeep Moab, 2019 BMW 335, 2018 Jeep Rubicon Recon, 2018 BMW 435i

- Occupation

- Broker/Owner

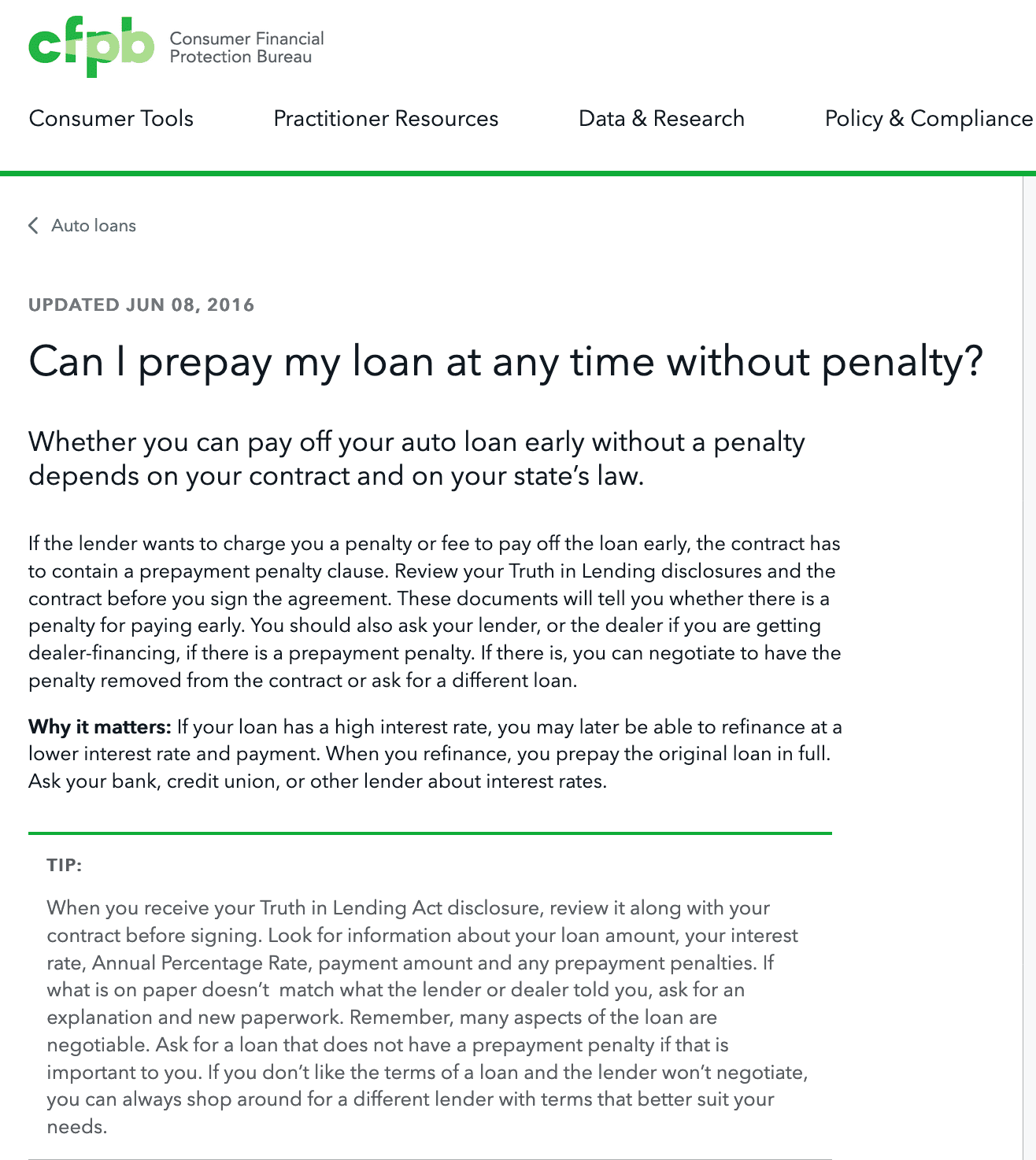

Again they can not tell you how many payments you must make and if they are they are breaking the law, RUN AWAY, screw themIf you sign a finance agreement contract stating that you would be in some cases there are penalties for early pay off on loans. That why you always read before you sign !

Sponsored