Sponsored

Some Random Guy

Well-Known Member

- Joined

- Sep 16, 2020

- Threads

- 61

- Messages

- 1,808

- Reaction score

- 2,178

- Location

- Washington

- Vehicle(s)

- 2022 JL Sport, 2022 Ford Mustang

- Occupation

- Comptroller

Capitalization cost is like purchase price. Residual value is expected value at end of lease. If you’ve got the credit/finances to be nimble, residual value can be “ignored”. Subtract the 2, divide by months to get an idea of how much your payment is principal payment vs “finance charges” (money factor can help compare the number)

If you can stomach the finance charges and purchase price/cap cost its probably alright. If you can’t, it probably isn’t. The residual value is irrelevant if you have the money/credit to buy out at then end. If it is too high, just let it go post-lease. If it is under what the jeep is worth, trade it in at the end and use the equity as downpayment on another lease or a purchase. Or just keep it knowing you’re “right-side-up” on a loan.

TLDR: post your residual on the lease offer to get more feedback.

If you can stomach the finance charges and purchase price/cap cost its probably alright. If you can’t, it probably isn’t. The residual value is irrelevant if you have the money/credit to buy out at then end. If it is too high, just let it go post-lease. If it is under what the jeep is worth, trade it in at the end and use the equity as downpayment on another lease or a purchase. Or just keep it knowing you’re “right-side-up” on a loan.

TLDR: post your residual on the lease offer to get more feedback.

Topless

Member

- Thread starter

- #3

The residual is 30278Capitalization cost is like purchase price. Residual value is expected value at end of lease. If you’ve got the credit/finances to be nimble, residual value can be “ignored”. Subtract the 2, divide by months to get an idea of how much your payment is principal payment vs “finance charges” (money factor can help compare the number)

If you can stomach the finance charges and purchase price/cap cost its probably alright. If you can’t, it probably isn’t. The residual value is irrelevant if you have the money/credit to buy out at then end. If it is too high, just let it go post-lease. If it is under what the jeep is worth, trade it in at the end and use the equity as downpayment on another lease or a purchase. Or just keep it knowing you’re “right-side-up” on a loan.

TLDR: post your residual on the lease offer to get more feedback.

Some Random Guy

Well-Known Member

- Joined

- Sep 16, 2020

- Threads

- 61

- Messages

- 1,808

- Reaction score

- 2,178

- Location

- Washington

- Vehicle(s)

- 2022 JL Sport, 2022 Ford Mustang

- Occupation

- Comptroller

Sooo, a $10,520 loan (cap cost - downpayment - residual cost) at 48 months with that payment comes out to a 32.7% interest rate. I feel like I’m missing something from your offer. Are you sure that is the cap cost and downpayment?

Also, I’ve been drinking. Math may be off.

Also, I’ve been drinking. Math may be off.

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

I leased my 80th in April, It seems about right to me.

One thing deceptive deal that many dealers advertise is the $0 down lease, but they mention in the fine print that it doesn't includes acquisition, or document fee, Tax, title, registration, etc. The 1st payment is also due as well at that time. The sales tax if applicable is also added to the monthly payment. My state charge sales tax on the fees as well. In MA $50K Wrangler usually eat $2000 of payment for TTL, fees, and 1st payment. A $2400 down payment might only be $500 cap reduction.

Jeep website also advertises many of the lease with 10% down, but to get those rates in MA, one would need to add another $2k (1st plus fees, TTL), plus that rate doesn't include sales tax for each monthly payment either.

One thing deceptive deal that many dealers advertise is the $0 down lease, but they mention in the fine print that it doesn't includes acquisition, or document fee, Tax, title, registration, etc. The 1st payment is also due as well at that time. The sales tax if applicable is also added to the monthly payment. My state charge sales tax on the fees as well. In MA $50K Wrangler usually eat $2000 of payment for TTL, fees, and 1st payment. A $2400 down payment might only be $500 cap reduction.

Jeep website also advertises many of the lease with 10% down, but to get those rates in MA, one would need to add another $2k (1st plus fees, TTL), plus that rate doesn't include sales tax for each monthly payment either.

Sponsored

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

One thing many people overlooked (or don't realize) in leases is that you pay interest on the total vehicle. The 30K residual is being charged interest for the entire lease duration. This is in addition to the interest paid on the difference between the capitalized cost and residual. CCAP interest rate for 48 month was right around 4%.

DarealUSA

Member

- First Name

- Kolja

- Joined

- May 22, 2021

- Threads

- 1

- Messages

- 22

- Reaction score

- 33

- Location

- Orlando, FL

- Vehicle(s)

- None

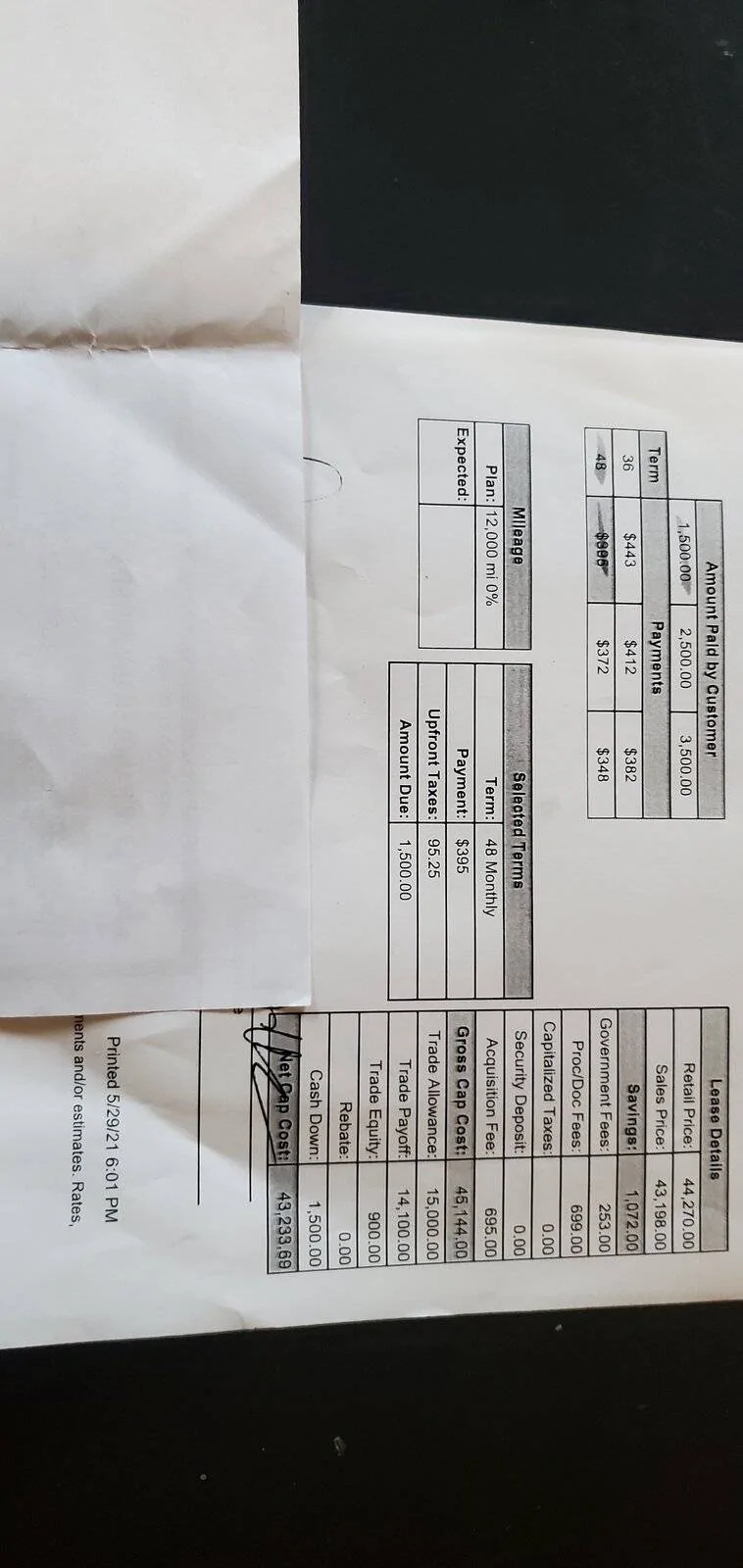

You are missing a few important numbers here to evaluate your deal. If you can post these, I'd be happy to help.My wife wants to lease a willys unlimted. The sticker is 44270.00 43198 with affiliates reward discount. $2400 down. 395 a month for 48 months. Is this a fair deal. Seems a little high. I havent leased in a few years.

- What's your Money Factor (if you don't have this, we can back into it)

- What's included in the downplay? Just cap cost reduction or does that include acquisition fees, dealer fees, etc

- Including taxes or without? What state / tax rate?

Take a look at the link below if you like. I pre-filled the leasehackr calculator with your numbers but many are still default.

https://leasehackr.com/calculator?make=Jeep&miles=12000&msd=0&msrp=44270&sales_price=43198&months=48&mf=.00100&dp=1425&dealer_fee=85&acq_fee=595&taxed_inc=0&untaxed_inc=0&rebate=0&resP=68.3939®_fee=400&sales_tax=9&demo_mileage=0&memo=&monthlyTax_radio=true&bmw_demo_25=true

Some Random Guy

Well-Known Member

- Joined

- Sep 16, 2020

- Threads

- 61

- Messages

- 1,808

- Reaction score

- 2,178

- Location

- Washington

- Vehicle(s)

- 2022 JL Sport, 2022 Ford Mustang

- Occupation

- Comptroller

Net cap cost seems off. It should be a $2400 reduction from the gross cap cost if I’m reading that right. Downpayment of $1500 cash plus $900 in trade-in equity.

So, my new math has you around 12.5% “interest”. Keep in mind the payments cover depreciation so this is purely finance charges against the “loan”. I personally don’t find that acceptable, I’d rather look into buying with a plan to sell. However, I don’t know your credit/finances. Years ago I may have been ok with this if I needed specific features of a vehicle for work.

Finally, most states calculate sales tax on a SALE by subtracting the trade in. I don’t think you get that on a lease, but I’m no expert.

edit: I ran numbers on my last lease and came out to 1.5% on my BRZ. More nightmares after that, but the finance charges were that low. I think my wife’s truck was also under 2%.

This technique can compare between lease and buy, but doesn’t make sense in accounting. The bank maintains ownership of the asset, so they are not “financing” the car. There is no interest on the residual value because you’re not borrowing money to pay the residual, only the depreciation. This is why they require broadened collision insurance, to protect their asset.One thing many people overlooked (or don't realize) in leases is that you pay interest on the total vehicle. The 30K residual is being charged interest for the entire lease duration. This is in addition to the interest paid on the difference between the capitalized cost and residual. CCAP interest rate for 48 month was right around 4%.

So, my new math has you around 12.5% “interest”. Keep in mind the payments cover depreciation so this is purely finance charges against the “loan”. I personally don’t find that acceptable, I’d rather look into buying with a plan to sell. However, I don’t know your credit/finances. Years ago I may have been ok with this if I needed specific features of a vehicle for work.

Finally, most states calculate sales tax on a SALE by subtracting the trade in. I don’t think you get that on a lease, but I’m no expert.

edit: I ran numbers on my last lease and came out to 1.5% on my BRZ. More nightmares after that, but the finance charges were that low. I think my wife’s truck was also under 2%.

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

The Money factor for a lease interest rate/2400. Why is it 2400? 100 of it is turning % into a decimal. So that leave 24. There is 12 months in year to turn into monthly rate, the remaining 2 is used for averaging.This technique can compare between lease and buy, but doesn’t make sense in accounting. The bank maintains ownership of the asset, so they are not “financing” the car. There is no interest on the residual value because you’re not borrowing money to pay the residual, only the depreciation.

To get the lease finance fee (Net capitalized cost + residual) x money factor. In this case it is (43233 + 30278) * MF. It may seem to odd to add those number, but is done this way because the averaging is built into the money factor. Effectively they are averaging the purchase price (after downpayment and fee) and the residual to come up average price over the lease. In this case (43233+30278) / 2 = 36,755.50 and this multiplied by the interest rate and divide by 12 figure out the monthly lease finance charge.

Sponsored

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

This website reiterates what I said above about you are paying interest on the entire vehicle's price.

https://www.leaseguide.com/lease08/

"Also be aware that you’re paying finance charges on both the depreciation and residual (the total of which is the negotiated selling price of the car). Remember, you’re tying up the leasing company’s money while you’re driving their car. They used their money to buy the car that you will drive while you lease. Technically, you’re paying finance charges on half of the depreciation (the average value) and all of the residual value for the term of the lease."

https://www.leaseguide.com/lease08/

"Also be aware that you’re paying finance charges on both the depreciation and residual (the total of which is the negotiated selling price of the car). Remember, you’re tying up the leasing company’s money while you’re driving their car. They used their money to buy the car that you will drive while you lease. Technically, you’re paying finance charges on half of the depreciation (the average value) and all of the residual value for the term of the lease."

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

In this deal, the $900 net trade and 1500 downpayment are almost paying the fees of the lease. It is short about $35. I would guess the reason why the Net cap cost does seem to add up, is that it includes sales tax on the taxable fees for your state.Heres what they gave her

Some Random Guy

Well-Known Member

- Joined

- Sep 16, 2020

- Threads

- 61

- Messages

- 1,808

- Reaction score

- 2,178

- Location

- Washington

- Vehicle(s)

- 2022 JL Sport, 2022 Ford Mustang

- Occupation

- Comptroller

I did a bad job finishing my thought. For comparison to a purchase, this is right. But if you’re comparing leases, it can be more productive to see how much of your payments are depreciation, and how much are finance charges. This is because the cap cost and residual can get moved around a lot. If you’re paying the same amount of depreciation, the finance fees can still be drastically different between 2 offers, resulting in very different payments. Something with a lower money factor can still cost you more over the course of the lease.The Money factor for a lease interest rate/2400. Why is it 2400? 100 of it is turning % into a decimal. So that leave 24. There is 12 months in year to turn into monthly rate, the remaining 2 is used for averaging.

To get the lease finance fee (Net capitalized cost + residual) x money factor. In this case it is (43233 + 30278) * MF. It may seem to odd to add those number, but is done this way because the averaging is built into the money factor. Effectively they are averaging the purchase price (after downpayment and fee) and the residual to come up average price over the lease. In this case (43233+30278) / 2 = 36,755.50 and this multiplied by the interest rate and divide by 12 figure out the monthly lease finance charge.

It is correct their money is tied up, however, the residual value is set to anticipate making a profit when selling your turn-in. So that is a hidden return for the leasing bank, and as a consumer you should not think of a lease like a loan against the whole vehicle. Focus on the depreciation, since that represents your value that gets used over the life of the lease term. Then, see if the extra costs (finance charges) make that worth it. If it is hard to stomach, consider buying with a plan to trade in a few years using the equity. You’re more likely to come out ahead, but you do take on some new risks (and a larger payment) You can’t just walk away at lease end if it is worth less than you anticipated on purchase day.This website reiterates what I said above about you are paying interest on the entire vehicle's price.

https://www.leaseguide.com/lease08/

"Also be aware that you’re paying finance charges on both the depreciation and residual (the total of which is the negotiated selling price of the car). Remember, you’re tying up the leasing company’s money while you’re driving their car. They used their money to buy the car that you will drive while you lease. Technically, you’re paying finance charges on half of the depreciation (the average value) and all of the residual value for the term of the lease."

All of this assumes your budget supports all options. If it doesn’t, leasing can allow us to have things normally out of reach. It also has some good protections built in for military members who might deploy or be moved overseas.

dgoodhue

Well-Known Member

- First Name

- Dave

- Joined

- Aug 22, 2020

- Threads

- 6

- Messages

- 586

- Reaction score

- 543

- Location

- Framingham, MA

- Vehicle(s)

- '21 80th JLU

I am not normally someone who leases, but I did this time because I am starting a new business this month with my fiance. I am providing the capital and she is going to run the businesses day to day operation, so I suspect I will be supplementing her income for about year as we grow the business. Instead of putting $20k down and having $600 monthly payment. I put $5k down & have a $350 lease and I kept $15k aside. I do plan on buying out the lease. I could have gotten a $330 month lease through Ally, which had a higher MF but a higher residual as well. The overall cost of the lease plus the residual buyout was going to be $5k more than the lease I chose with the lower MF. I am sure most customers don't choose the higher lease payment.But if you’re comparing leases, it can be more productive to see how much of your payments are depreciation, and how much are finance charges. This is because the cap cost and residual can get moved around a lot. If you’re paying the same amount of depreciation, the finance fees can still be drastically different between 2 offers, resulting in very different payments. Something with a lower money factor can still cost you more over the course of the lease.

Some Random Guy

Well-Known Member

- Joined

- Sep 16, 2020

- Threads

- 61

- Messages

- 1,808

- Reaction score

- 2,178

- Location

- Washington

- Vehicle(s)

- 2022 JL Sport, 2022 Ford Mustang

- Occupation

- Comptroller

This makes a lot of sense, and a good choice between the 2 options. I still don’t like the rate, but admittedly I don’t know what a good deal is on a wrangler lease.I am not normally someone who leases, but I did this time because I am starting a new business this month with my fiance. I am providing the capital and she is going to run the businesses day to day operation, so I suspect I will be supplementing her income for about year as we grow the business. Instead of putting $20k down and having $600 monthly payment. I put $5k down & have a $350 lease and I kept $15k aside. I do plan on buying out the lease. I could have gotten a $330 month lease through Ally, which had a higher MF but a higher residual as well. The overall cost of the lease plus the residual buyout was going to be $5k more than the lease I chose with the lower MF. I am sure most customers don't choose the higher lease payment.

I spent a lot less on my 2 leases for finance charges, including on a pickup with a similar MSRP. We did get a conquest incentive, though. Our payments were around $300 with no downpayment, extra miles, and only a 2 year term.

Sponsored