CBR2200

Active Member

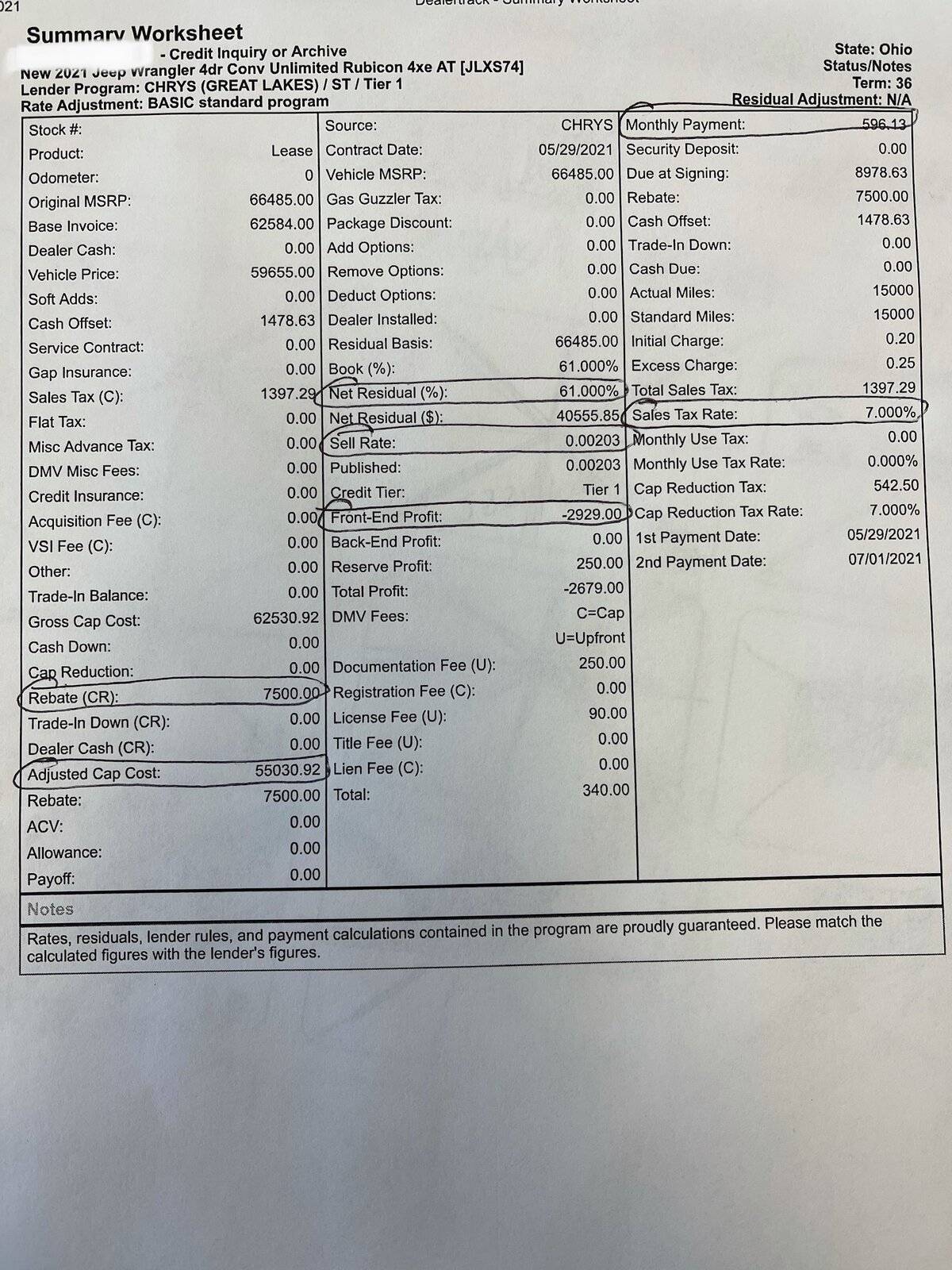

Can someone verify the 4xe residual with CCAP please? And is that based on MSRP or the negotiated cap cost? My dealer is telling me it's 60% of the negotiated cost for a 3yr 15k mile 4Xe Rubicon.

Sponsored

Rubicon 36/15 is 61% rv buy rate mf is .00203 acquisition fee is also waived this month so make sure they don’t charge you that.Can someone verify the 4xe residual with CCAP please? And is that based on MSRP or the negotiated cap cost? My dealer is telling me it's 60% of the negotiated cost for a 3yr 15k mile 4Xe Rubicon.

Disposition fee is what you will pay when you turn in the vehicle.Does the acquisition fee have any synonyms the dealer might use such as disposition fee or service fee...can someone tell me what the acquisition fee would be if they hadn‘t waived it?

You’re paying about $23k over the course of the lease.I think this could help. We are similar vehicles, terms, and everything. I’m in Ohio (7% tax).

Here is a written quote from my dealer. 61% RV, .00203 MF.

Curious what people think of this write up, and whether there’s anything fishy in here or if it’s a good deal. Also hoping it helps you since we are a similar deal.

I get a new vehicle every 3 years. I put $0 down and drive ~$60k-$70k vehicles for $500-$600/month. At the end of the lease, sell the vehicle for a $10k profit.To help compare finance charges and interest, I pulled an estimate from my bank. A $50k loan clocks in at 1.89% for my bank. That is just under $2500 interest over the course of the 5 year loan. The payment is $875 though.

This is out of reach for some budgets, so the lease becomes tempting.

This is why I recommend comparing based off capitalization cost minus residual (aka, the depreciation). Think of it from the bank’s perspective. They hand you something worth $60k, receive payments every month, then are guaranteed to get back $40k (they’ll get there with mileage charges, termination fees, or wear-and-tear charges if the vehicle isn’t worth the residual). If those payments add up to a significantly higher amount than $20k, they’re making a lot of money. They should expect single digit rates of return in my opinion, and they make deals that do.

If you’re paying over 10%, you’re doing it for a scarce asset or being taken for a ride. The first might be ok if you really want/need it, you’re an adult and can decide if this applies to you; but the second is not acceptable.

Question on that approach.I get a new vehicle every 3 years. I put $0 down and drive ~$60k-$70k vehicles for $500-$600/month. At the end of the lease, sell the vehicle for a $10k profit.

I’ve historically agreed with your math and purchased all my vehicles. After leasing a Wrangler and seeing the profits at the end of the lease, this beats the heck out of buying ?

You’ve struck on how to win with leases. If you can come out ahead of residual, it can work well. My BRZ actually appreciated in value, so I had roughly $15k in “equity” by exercising my purchase option (or trading it in before expired on a new purchase/lease where the dealership exercised my option).I get a new vehicle every 3 years. I put $0 down and drive ~$60k-$70k vehicles for $500-$600/month. At the end of the lease, sell the vehicle for a $10k profit.

I’ve historically agreed with your math and purchased all my vehicles. After leasing a Wrangler and seeing the profits at the end of the lease, this beats the heck out of buying ?

You are either buying it out yourself (which requires cash on hand or a used car loan) or allowing a dealership to exercise the option for you, potentially as part of a trade-in. The residual will generally not be lowered after signing, unless you do an extension or something.Question on that approach.

So you make all 36 payments then at the end you buy the vehicle at it's residual value as noted in the lease agreement? And after buying it you immediately sell it and are able to make profit? Or are you buying it less than the residual amount? If so how are you able to do that? Since it's already spelled out in the contract I don't see how or why the dealer would negotiate that.

I thought about paying with cash on hand and then flipping it, or possibly going to a dealer on trade.You are either buying it out yourself (which requires cash on hand or a used car loan) or allowing a dealership to exercise the option for you, potentially as part of a trade-in. The residual will generally not be lowered after signing, unless you do an extension or something.