CatskillsAlex

Well-Known Member

- First Name

- Alex

- Joined

- May 8, 2018

- Threads

- 3

- Messages

- 828

- Reaction score

- 2,852

- Location

- Upstate NY + NYC

- Vehicle(s)

- 2021 2-door Rubicon

Thank you for taking the time to lay this out in clear terms. Agree that the leasing vs buying debate seems to be vastly misunderstood/misinterpreted/misrepresented. Heck, I work in finance and I still wouldn’t claim I have a clear understanding of all those dynamics, mostly because I’ve heard so much conflicting info over the years. The way you articulated your thought process was very helpful - thanks again.Looks like there's some severe misunderstandings on leasing:

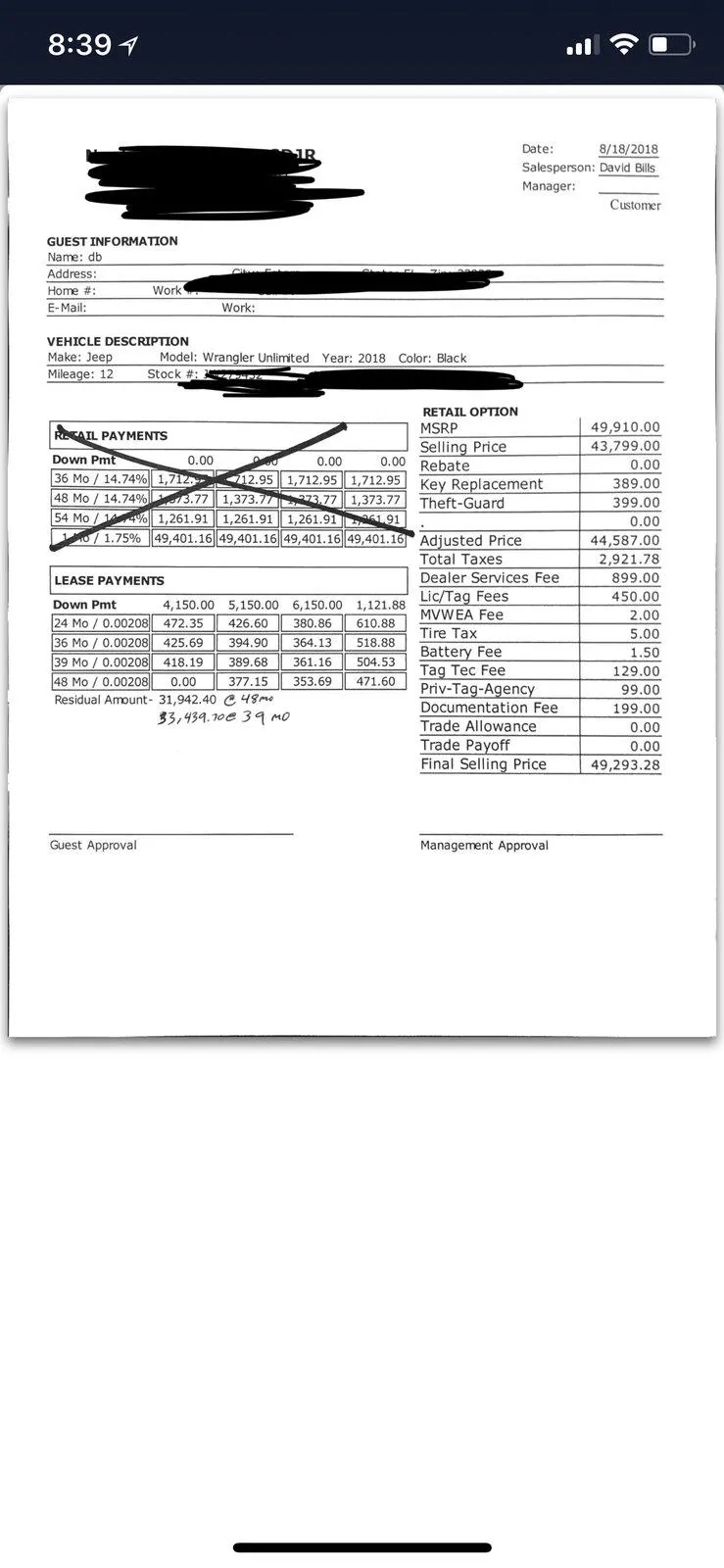

When you finance a car you are taking a specific amount of money and paying for it over a specific period of time. So let's take a $50k car for example.

Let's assume you finance with nothing down. You can choose the length of the term. Let's pick 60 months. During the first month you owe $50k so you will pay interest on $50k plus some amount towards the equity paydown. Every month you will owe less on the car so the interest portion of your payment is less because the principal balance is lower thus leaving more of your payment towards the principal paydown. Because we chose 5 years, on average you will have paid down approximately 20% of the initial price every year (slightly less in earlier years and slightly more in final years but negligible difference on 5 year loan). But because you are paying off so much of your car so fast the amount you still owe drops rapidly and thus the interest amount does as well.

The downside is you are artificially choosing 5 years. Realistically the car still has value after 5 years so you've actually paid down more of the cars value than you used, effectively building up equity. But you are not building equity in the sense that the asset has gone up in value, simply that you overpaid for the amount you used. Jeep figures the Wrangler Rubicon will be worth approximately 68% of its initial value after 3 years (residual). So they amortize the payment to match that.

Using the 5 year financing method above, after 3 years you only owe $20k on your Jeep, but Jeep thinks that car might be worth $34k at that time. So instead of having you pay down so much and then giving you a refund of $14k at lease end ($34k - $20k prinicipal left using a 5 year finance structure) they choose a point in the future and match your amortization schedule so your principal equals what they think is the value of the car at that future point. To have a $50k car have $34k remaining principal in 3 years, you would need to spread the amortization over 9 years.

So using Jeep's numbers, their lease is exactly like financing the car over a 9 year term but with the option to give the car back after 3 years because the principal remaining equals what Jeep thinks it will be worth.

Some of you might think its crazy to finance a car over 9 years but all you are doing when you finance it for a shorter period of time is using your car as a savings account. You are paying down the amount you owe faster than its depreciating and then if you sell, you'll recoup that extra money. But considering the low interest rates today, you are putting money into a 2% interest savings account. You could just as easily pay the actual amount that the car is depreciating and the "extra" money you would otherwise have paid to pay down your loan faster than depreciation, you could freely invest in anything you want. The probability that the best and highest risk adjusted return in the universe of investable assets is coincidentally the car you want to buy is unlikely.

A car is a depreciating asset and therefore has 2 costs, the amount of the value that depreciates during the time you own it and the interest on the asset for the time you own it. Paying more than that is fine, but there's no magic to it. It's exactly the same as a lease. Imagine walking into a hotel and asking how much it will cost to stay there for the next 2 years. The manager adds up the nightly rates and gives you the total. You could pay the total that matches the time you will use the hotel or you could tell the manager that you would like to pay a lot more than the total but have the difference refunded to you at the time you check out. That's the difference between financing a car using a artificially short amortization (4-5 years) and leasing with a more realistic amortization (based on objective measures of depreciation). If you do choose to pay for exactly the hotel cost, it makes no difference to the manager if you pay it every day or the entire amount upfront or any combination thereof. Same with a lease. You are paying for the depreciation for the duration of the lease plus interest on the remaining principal. If you choose to pay that upfront or monthly just affects your payments and barely affects the total amount you pay (I wrote barely because obviously with payments there os more principal outstanding during the lease term so total interest payment is a bit higher to cover interest on the higher balance).

Sometimes people act like these are 2 radically different mechanisms. Its the exact same thing just with different loan terms. The only real differences are:

1) Any interest rate difference (sometimes the lease interest rate or finance interest rate can be higher/lower depending on manufacturer or bank programs)

2) The extra protection of having the right to walk away at lease end. If car is worth more you can still sell it yourself but if it has depreciated equal to or greater than the lender's projection you get to "sell" at that higher price by turning the car in.

3) Any tax implications (usually if you have a business)

All the other stuff of extra fees etc. is nonsense. Anyone can request any fees they want and it's up to you to say no. There should be no difference in negotiated price or fees should you choose to lease or buy. Even the term buy is misleading, you are borrowing under an accelerated pay-back window.

As for keeping the car at the end of the lease. That goes back to point 1 above regarding interest rate differences. Financing upfront may be more advantageous if you can lock in a lower interest rate for the entire term of the loan versus splitting the loan into 2 portions with 2 different rates. The lease rate for the initial term and then the used car interest rate for the term following the buyout.

He's paying interest on the entire amount he is borrowing. When you lease you are borrowing the entire vehicle for 3 years (not just the value the car will lose while you own it) and therefore pay interest on the entire outstanding principal every month you still have the car. Just like if you finance a car, the first month you will pay interest on the entire value of the car and every month it will go down.

Sponsored