DietStartsMonday

Member

- Thread starter

- #1

Alright so I've read a lot of posts on here which really helped me see the value in leasing a car being how well Wranglers hold theirvalue.

I've been searching for about a month now and trying to come up with the best deal...

I've got a deal in place and was hoping to get some opinions on it.

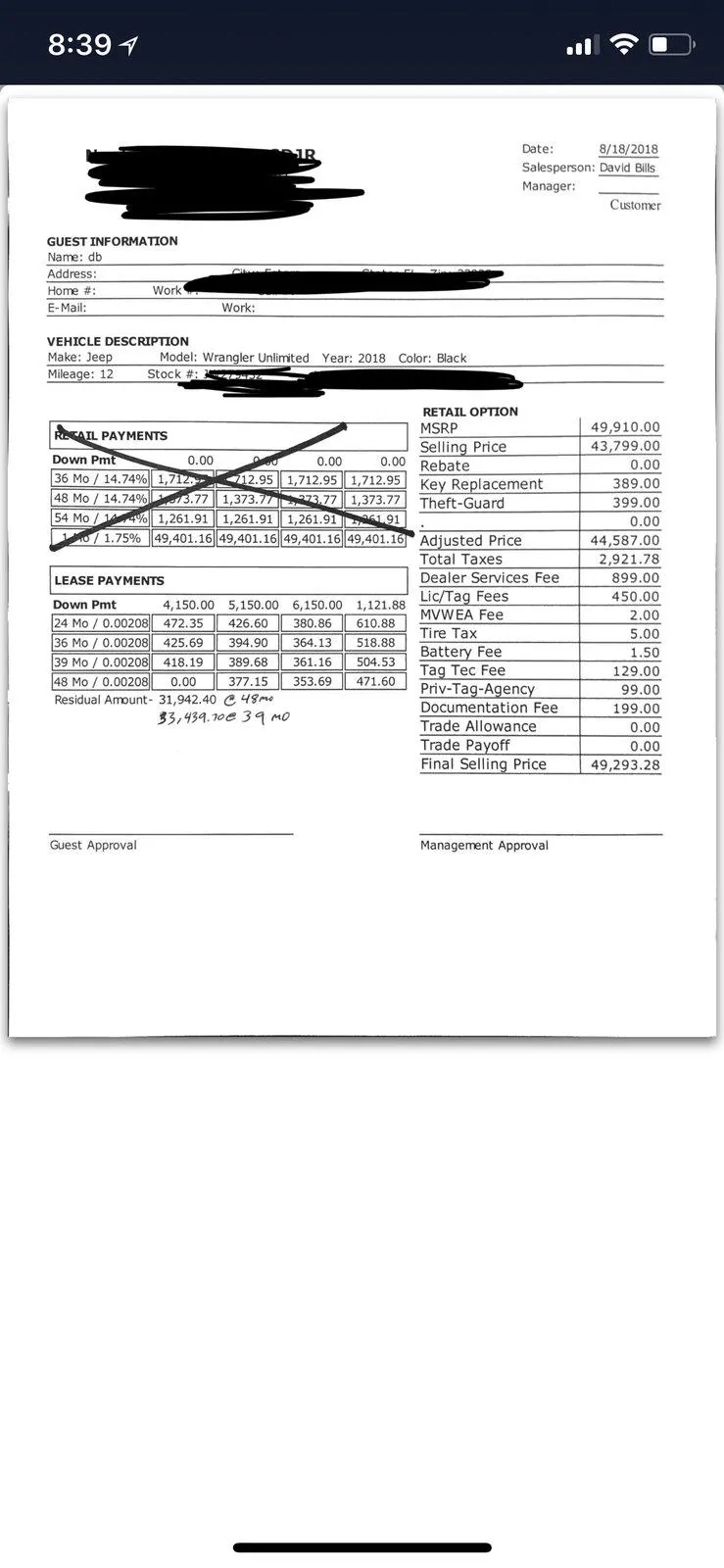

JEEP JLUR

MSRP: $47,910

Invoice: $43,799 (9% below msrp)

MF: .00208 (4.99% APR)

Term: 48/10

RV: 64% ($31,942)

Total Due at signing: $4,150

Mo. Payment: $400

I've attached the breakdown sent by thedealership... i've been using leasehackr to help base the numbers and with everything I think I’ve learned so far something still doesn't seem right...

From what I added up, all of the "dealer fees" add up to $1,784.5 which the sales manager added up to $2049.00; so right there that doesn't make sense; maybe just bad

Based off what they broke down, they have a final sales price of $49,293. Here's where I think they are trying to pull the wool over my eyes... How does the final sales price become $1383 more than MSRP

Out of the $4150, I took the $1784.5 out for dealer fees which leaves $2365.5 that should be applied to net cap cost.. if i'm assuming correct, that 2365.5 should be directly deducted from the invoice of $43,799; no? All that I should be responsible for is the tax on net cap cost..

So if you take 41433.5 (new invoice # after Down Payment) - 31942 (RV) = $9,491.5 (Depreciation)

IDK, am i missing something? This is the first lease i've ever truly looked into the numbers to understand the math side of things and all it really makes me realize how corrupt dealerships are... i mean i get they need to make money but their approach in doing so is in hopes that the consumer is blind enough to just look at the mo. payment....

I'd love to get some feedback on this deal and possibly a strategy to best close this deal.

I've been searching for about a month now and trying to come up with the best deal...

I've got a deal in place and was hoping to get some opinions on it.

JEEP JLUR

MSRP: $47,910

Invoice: $43,799 (9% below msrp)

MF: .00208 (4.99% APR)

Term: 48/10

RV: 64% ($31,942)

Total Due at signing: $4,150

Mo. Payment: $400

I've attached the breakdown sent by thedealership... i've been using leasehackr to help base the numbers and with everything I think I’ve learned so far something still doesn't seem right...

From what I added up, all of the "dealer fees" add up to $1,784.5 which the sales manager added up to $2049.00; so right there that doesn't make sense; maybe just bad

Based off what they broke down, they have a final sales price of $49,293. Here's where I think they are trying to pull the wool over my eyes... How does the final sales price become $1383 more than MSRP

Out of the $4150, I took the $1784.5 out for dealer fees which leaves $2365.5 that should be applied to net cap cost.. if i'm assuming correct, that 2365.5 should be directly deducted from the invoice of $43,799; no? All that I should be responsible for is the tax on net cap cost..

So if you take 41433.5 (new invoice # after Down Payment) - 31942 (RV) = $9,491.5 (Depreciation)

IDK, am i missing something? This is the first lease i've ever truly looked into the numbers to understand the math side of things and all it really makes me realize how corrupt dealerships are... i mean i get they need to make money but their approach in doing so is in hopes that the consumer is blind enough to just look at the mo. payment....

I'd love to get some feedback on this deal and possibly a strategy to best close this deal.

Sponsored